- Additional Medicare Tax- In a nutshell, an extra 0.9% on earned income exceeding $250k for couples, $200k for individuals.

- Net Investment Income Tax- 3.8% of net investment income or MAGI over $250k for a couple, $200k for individual filers. Tea Partiers went nuts over this but hey, should we tax poor working stiffs or passive (i.e. nonworking) income?

- Top tax rate is now 39.6%- Put the guns away. This applies only to taxable income over $450,000 for a couple. And is still a far cry from the highest historical marginal rates >90%. I only have two clients who are affected by this and I guarantee you it will not affect the kind of breakfast cereal they eat.

- Capital Gains & Dividends- for some folks the top rate will increase from 15 to 20%. Why isn't this passive income taxed at the same rates as earned income???

- Medical Deductions- unless you or or spouse are 65 or older, the hurdle for deductibility is increased from 7.5 to 10%. But corporations, which the Supreme court has affirmed are people, can deduct every penny. I see.

- Yay, Person Exemptions!- increased to $3900, with exceptions.

- Itemized Deductions Restricted- if you make over $250k & are single & other details.

- Same Sex Couples- Can file as married if legally married in a state, even if no longer living there.

- FSAs- Can't divert more than $2500/yr into these.

- Plug-in vehicle Credit expired in 2012, thankyou big oil.

- Home office deduction- simplified

- Standard Mileage Rate- 56 cents for business, 24 cents for medical care or moving.

"Ensuring your prosperity in the years to come using resources you have today"

Monday, February 24, 2014

Not a Myth- What's New for 2013 Tax Filers

Here's a list of significant and/or interesting changes handed down by IRS. This is by no means a complete list. Please consult with your tax expert or at least Publication 17.

Friday, February 14, 2014

IRS is never helpful

Just a reminder, these headings are Financial Myths unless otherwise noted. IRS can actually be very helpful, if you know where to look. And it should get better, thanks to TAP, the new Taxpayer Advocacy Panel made up of 73 volunteers around the country. I applied for this panel but they ended up selecting no one from Oregon, probably because of me; my three suggestions for improving IRS customer service were:

- Leave

- Me

- Alone

No doubt they assumed everyone here is nuts and passed us over entirely. Here's the link to the announcement, if you're interested in sending comments to TAP: http://www.irs.gov/uac/Newsroom/Taxpayer-Advocacy-Panel-Members-Selected-2014

Another recent sort of friendly gesture is Publication 910, "IRS Guide to Free Tax Services". To save you the effort of looking at all 27 pages, here are the sweet spots, in my opinion:

- pp. 1-3- IRS.gov. Yes, their website is easy to navigate and full of robustness.

- p. 6 - tax advice for seniors. Free.

- p. 9 -FreeFile, the online tax return preparation and filing system which, they claim, 40 million taxpayers have used thus far.

- This is cool. At benefits.gov you can search for the hundreds of potential benefits programs that might apply to you.

- p.12 -Guide to free tax services

- p.18 -Nonprofit and Small Business resources. I've used this extensively in my Treasurer roles at nonprofits.

So yes, Matilda, even the IRS can be warm and fuzzy.

Tuesday, February 4, 2014

One of the greatest financial tools available in Oregon is going away on 2/24

In a fascinating January 28 interview with James Montier (of Grantham Mayo van Otterloo [GMO] with $10 mil. account minmums!), Robert Huebscher teases out some thoughts & facts that warrant further study, if you would like to take the time to read it. (see What Worries Me Now) But I'll save you some time with this bullet-point list:

- At the bottom of the market in 2009 "accounting authorities suspended FASB rule 157 . . . all of a sudden, financial institutions could lie with impuity" about their declining asset values. Is this one factor in the market run up? Possibly. But FASB157 was replaced by ASC820 which, by my reading, uses very reasonable asset valuation formulas. And won't financial institutions continue to lie with impunity anyway as long as they remain almost entirely self-regulating? This is an important issue because the techniques used to assign a market value to assets and income streams directly affect stock prices and, therefore, your retirement account balances.

- He acknowledges the economic fact that government austerity is "likely to drag down profits and that remains a major source of concern". The prevailing notion that taxes vanish into a black hole is so tired and, well, stupid that I'm glad to see a major fund manager dispel it. Government belt tightening- just for the sake of belt tightening, I might add -slows the circulation of money & hurts the economy.

- Montier recognizes that "this is the purgatory of low returns". He goes on to say that "the perfect dry-powder asset would . . . give you liquidity, protect you from inflation, and it might generate a little bit of return". And then, "Right now, of course, there is nothing that generates all three of those characteristics".

It is this last assertion with which I heartily disagree. What if there were an asset which:

- Was principal guaranteed, every year. Not ever losing money enhances long term returns.

- Allowed you to use a "5% rule" or greater, depending on your age, (instead of the traditional "4% rule"* which is now considered excessive) for withdrawals

- Every year that you delay taking withdrawals, for up to 20 years, your income amount would increase by 7.2%

- You have 10-20% liquidity annually

- 100% liquidity of principal plus interest in the event of death or 10 years.

*The lifetime retirement account withdrawal rate that assures you won't run out of money before your life expectancy. It has recently been revised to 3%.

Tuesday, January 7, 2014

Tuesday, December 17, 2013

It's a great time to Hire a Veteran

IRS to Employers: Hire Veterans by Dec. 31 and Save on Taxes

IRS Special Edition Tax Tip 2013-15, December 3, 2013

If you plan to hire soon, consider hiring veterans. If you do, you may be able to claim the federal Work Opportunity Tax Credit worth thousands of dollars.

You must act soon. The WOTC is available to employers that hire qualified veterans before the new year.

Here are six key facts about the WOTC:

- Hiring Deadline. Employers hiring qualified veterans before Jan. 1, 2014, may be able to claim the WOTC. The credit was set to expire at the end of 2012. The American Taxpayer Relief Act of 2012 extended it for one year. The WOTC expires on Dec. 31, 2013.

- Maximum Credit. The tax credit limit is $9,600 per worker for employers that operate a taxable business. The limit for tax-exempt employers is $6,240 per worker.

- Credit Factors. The credit amount depends on a number of factors. They include the length of time a veteran was unemployed, the number of hours worked and the amount of the wages paid during the first year of employment.

- Disabled Veterans. Employers hiring veterans with service-related disabilities may be eligible for the maximum tax credit.

- State Certification. Employers must file Form 8850, Pre-Screening Notice and Certification Request for the Work Opportunity Credit, with their state workforce agency. They must file the form within 28 days after the qualified veteran starts work. For more information, visit the U.S. Department of Labor’s WOTC website.

- E-file. Some states accept Form 8850 electronically.

For more about this topic, visit IRS.gov and enter ‘WOTC’ in the search box.

Additional IRS Resources:

- Work Opportunity Tax Credit Extended

- Work Opportunity Tax Credit - Frequently Asked Questions and Answers

- Form 8850, Pre-Screening Notice and Certification Request for the Work Opportunity Credit

Learn the primary myths and truths about Retirement!

Retirement classes begin again on January 14th at PCC SE Center in Portland:

- Go to this link, http://tinyurl.com/knosyaa

- check the location, dates and times to see if they work for you

- If they do, click on "Registration" and set up an account

- then, register for my class!

Please feel free to call or email if you would like details about the class content, the substantial packet that you get, or if you just wonder whether the class will help you with your particular situation. If it won't help, I'll be the first to tell you. Make this a New Year's resolution!

Peace and Love,

Gary

Tuesday, November 26, 2013

WARNING: Not a Myth- Investment Scams of 2014

We Oregonians are blessed to have a relatively healthy investment watchdog on our team, the Oregon Division of Finance and Corporate Securities (DFCS). Among other valuable resources, their website includes License Holder Searches for a whole range of financial services providers, from banks & prepaid funerals to pawnbrokers & payday lenders.

Every year about this time they highlight the worst of the financial scams for the year & project warnings for the next year. Here's the link: http://altarum.org/health-policy-blog/a-closer-look-at-the-slowdown-in-health-care-price-inflation

Because the Internet blurs state lines, the DFCS includes all states in their list. The most notable risk is new, the result of the JOBS act which loosens the rules companies have to follow to raise capital. A double edged sword, this ability to sidestep Wall Street is great but it also means less scrutiny of each offering. Personally, how the SEC could exercise less scrutiny seems impossible without the liberal use of narcotics.

Before you invest in something that sounds too good to be true, do your research. Or hire me to do it for you. As DFCS administrator David Tatman says, don't invest more than you "can afford to lose" in these types of companies. I would go further: Don't invest more than you would be happy to lose.

Every year about this time they highlight the worst of the financial scams for the year & project warnings for the next year. Here's the link: http://altarum.org/health-policy-blog/a-closer-look-at-the-slowdown-in-health-care-price-inflation

Because the Internet blurs state lines, the DFCS includes all states in their list. The most notable risk is new, the result of the JOBS act which loosens the rules companies have to follow to raise capital. A double edged sword, this ability to sidestep Wall Street is great but it also means less scrutiny of each offering. Personally, how the SEC could exercise less scrutiny seems impossible without the liberal use of narcotics.

Before you invest in something that sounds too good to be true, do your research. Or hire me to do it for you. As DFCS administrator David Tatman says, don't invest more than you "can afford to lose" in these types of companies. I would go further: Don't invest more than you would be happy to lose.

Monday, October 21, 2013

The Annuity That All Annuity-Haters Buy

At one point in my planning process I show my clients the Red-Green spectrum of all possible places they can put their money, from bank savings accounts & CDs to credit default swaps & REITs. I ask them if anything on the spectrum is off the table, any options they absolutely would not consider. Most of my clients are my age or older and so are risk averse. Most aren't interested in "Red" money like oil well leases & options. And a few cross off annuities. They hate and/or fear annuities because of what they've "heard" (not because of what they know). I don't argue. I take everything off the table they don't like.

Then we drill down into their specific desires, in most cases:

Then we drill down into their specific desires, in most cases:

- Protection of their investment principal- they do not want any backsliding in their portfolio

- Inflation protection- a minimum rate of return at least adequate to keep up with inflation so their purchasing power isn't eroded over time. They want to participate in the upside of the market but not in the downside

- Some tax advantages- it adds insult to injury to earn half a percent on a CD and then have to pay income taxes on it to boot.

- Keeping their Social Security benefits nontaxable.

- Some income guarantees- if they've attended one of my retirement classes they've learned that outliving one's income is one of the three greatest retirement risks. They would like an income they cannot outlive.

- Liquidity if a crisis occurs, like having to go into a nursing home or the death of a spouse.

Then I have to tell them that they've taken off the table the best tools I have for accomplishing all those goals: annuities. That is, the right annuities used in the right way with the right amount of their funds.

Take for example Social Security. Social Security is a stream of payments, i.e., an annuity. And a darn good one at that, if it is applied for optimally. Everyone who is eligible for this stream of payments has "bought" it with their payroll taxes. (In fact, some people are eligible for it who have never even paid so much as a cent for it: nonworking spouses.) I have yet to meet anyone who was "principled" enough to decline Social Security because it is an annuity.

Friday, September 20, 2013

Purple Unicorns can make you RICH!

Ken Fisher, Jonathan Pond, Suse Orman, Jim Cramer the list goes on of financial entertainers who propagate enough truth to be useful and alluring but also enough myth to be devastating. All of them lost their readers/clients tons of money in the last crash and will do so again in the next one coming up. Like a lot of questionable politicians who are inexplicably voted back into office over and over, they benefit mightily from a highly distracted populace with very short memories. They are what I call Financial Pornographers. None of them hold themselves to a fiduciary standard like I do.

I know that initially this sounds harshly cynical, a glaring violation of Dan Pink's well-documented ABC sales principles (Attunement, Buoyancy & Clarity). But bear with me. We're in the Attunement phase here. I'm attempting to connect with and deconstruct the magical thinking Wall Street has injected into our culture.

One aspect of this magical thinking is how investors decide to whom to give their money. When I meet with potential clients I ask them why they picked their current adviser and why they are leaving. I do this to dispel any delusions about their attraction to me, and, to avoid the mistakes the former adviser made. Almost invariably they were attracted by the adviser's "success", as evidenced by $1000 suits, expensive cars & high-rent office. (Wes Rhodes is a classic local example. Bernie Madoff is an infamous national example.) I ask, "Well who do you think paid for all that?". Even if they don't come right out and say it I can see the wheels turning, "We did.". (The mythological belief is that the stock broker has been a great success with his own money and now wants to share that success with little ol' you.) And almost invariably my new clients left their broker because of excessive fees and performance that's worse than unmanaged indexes.

The complicated, circuitous narrative the entertainers propagate for risk-taking versus safety might as well be: Well, in the back room we have a team of very skillful gnomes feeding magic mushrooms to our herd of purple unicorns, which then excrete the gains you'll experience. Wow! That's exciting just to make up! I almost want to say, "Uh huh. Ok. Sign me up!" Unfortunately, in most cases there are no purple unicorns, just ordinary bulls eating ordinary hay and excreting ordinary . . .ahem.

I know that initially this sounds harshly cynical, a glaring violation of Dan Pink's well-documented ABC sales principles (Attunement, Buoyancy & Clarity). But bear with me. We're in the Attunement phase here. I'm attempting to connect with and deconstruct the magical thinking Wall Street has injected into our culture.

One aspect of this magical thinking is how investors decide to whom to give their money. When I meet with potential clients I ask them why they picked their current adviser and why they are leaving. I do this to dispel any delusions about their attraction to me, and, to avoid the mistakes the former adviser made. Almost invariably they were attracted by the adviser's "success", as evidenced by $1000 suits, expensive cars & high-rent office. (Wes Rhodes is a classic local example. Bernie Madoff is an infamous national example.) I ask, "Well who do you think paid for all that?". Even if they don't come right out and say it I can see the wheels turning, "We did.". (The mythological belief is that the stock broker has been a great success with his own money and now wants to share that success with little ol' you.) And almost invariably my new clients left their broker because of excessive fees and performance that's worse than unmanaged indexes.

The complicated, circuitous narrative the entertainers propagate for risk-taking versus safety might as well be: Well, in the back room we have a team of very skillful gnomes feeding magic mushrooms to our herd of purple unicorns, which then excrete the gains you'll experience. Wow! That's exciting just to make up! I almost want to say, "Uh huh. Ok. Sign me up!" Unfortunately, in most cases there are no purple unicorns, just ordinary bulls eating ordinary hay and excreting ordinary . . .ahem.

Friday, August 23, 2013

Nobody is using IRS Sec. 101(a) plans!

Well, this post title is a myth. Lots of people own Sec. 101(a) plans. Most just don't know it. The sad thing is, though, except by the wealthy, the provisions of Sec. 101(a) are rarely fully used. If you've already google searched Sec. 101(a) you know that this post is just in time for September, which is Life Insurance Awareness Month.

Sec. 101(a), along with other tax code provisions, delineates some of the amazing tax and asset-leveraging advantages of life insurance. Reminds me of a comedian who wondered about the persuasive shyster who invented life insurance: "Hey, pay me $100 and then when you die I'll give you back $200!". I think the reason people are turned off about life insurance is because of life agents, not the products they sell. It doesn't help that financial "gurus" like Suze Orman have been telling people for years to buy term, not whole life (although she has changed her tune lately). But that advice only takes narrow advantage of Sec. 101(a)(1). It's like buying an umbrella but not being able to open it unless you're dead.

What can you do with the latest life insurance hybrid products these days? Here's a partial laundry list, (all of which of course are totally contingent upon the insurer, the specific product design, policy provisions, your health and family history, etc.):

I'm not sure how I feel about all this because, originally, tax advantages were given to life insurance for the benefit of destitute widows and orphans. Now it seems the wealthy are the main beneficiaries of these provisions. Which is why on an annual basis Congress considers attacking them or at least means testing them to get more tax revenue. But my job is do give you the best advice I can under current laws, regulations and economic conditions. You should take it.

Sec. 101(a), along with other tax code provisions, delineates some of the amazing tax and asset-leveraging advantages of life insurance. Reminds me of a comedian who wondered about the persuasive shyster who invented life insurance: "Hey, pay me $100 and then when you die I'll give you back $200!". I think the reason people are turned off about life insurance is because of life agents, not the products they sell. It doesn't help that financial "gurus" like Suze Orman have been telling people for years to buy term, not whole life (although she has changed her tune lately). But that advice only takes narrow advantage of Sec. 101(a)(1). It's like buying an umbrella but not being able to open it unless you're dead.

What can you do with the latest life insurance hybrid products these days? Here's a partial laundry list, (all of which of course are totally contingent upon the insurer, the specific product design, policy provisions, your health and family history, etc.):

- Pass unneeded IRA money to your kids or grandkids completely tax-free, multiplied 2-3 fold

- Pay life insurance premiums with tax-free dollars

- Earn 5-8 times current CD interest rates, also tax-free

- Guarantee that your children can pay for college, whether you live or die

- If you're already maxing out a Roth, build a supplemental retirement nest egg to provide future tax-free income

- Participate in a variety of market indexes with your worst-case annual loss being . . . zero

- Have coverage that will actually be in force when you die. Very very very few term policies ever pay off because they usually lapse (due to gargantuan premium increases).

- Buy more coverage cheaper than term over your lifetime. Go ahead. Compare buy-term-and-invest-the-difference with an equity indexed universal life policy.

- Have a source for low or no interest loans if you need a house down payment, want to take a trip, or make a major purchase. And don't pay it back until you die.

I'm not sure how I feel about all this because, originally, tax advantages were given to life insurance for the benefit of destitute widows and orphans. Now it seems the wealthy are the main beneficiaries of these provisions. Which is why on an annual basis Congress considers attacking them or at least means testing them to get more tax revenue. But my job is do give you the best advice I can under current laws, regulations and economic conditions. You should take it.

Saturday, August 17, 2013

WHEN THE MARKETS ARE BOOMING, EVERYONE'S A GENIUS

I won't make any friends with that blog title. But it's been my experience with every market run up; the phones stop ringing, annual reviews are postponed, & Jim Cramer is a hero again as his disciples forget how much of their money he lost, now that he has them "back to even".

Happily, there are exceptions. Finally the public is realizing the illusory nature of the market run-up, cognizant that their own household micro-economy has not followed suit. Could it be the approximate $100 billion in funny money per month that the Federal Reserve (Fed) is pumping into the markets? Probably. And the best evidence yet that this is the case is the recent market drop due to falling unemployment rates. Yes, you read that right.

Usually falling unemployment means higher consumer disposable income and therefore higher spending which in turn buoys corporate earnings, causing stock values to rise. So why are they falling instead?? Because Wall Street fears the Fed will back off on its Monopoly money stimulus as the jobs picture "improves" (It's not improving, not really. They're just measuring it differently.). Less money chasing the same securities will cause stock prices to fall. Hence the defensive sell off now.

Wall Street's mantra is "You don't want to miss the best days of the market, so keep fully invested". My mantra is, "It is far more important to avoid the worst days!"

Happily, there are exceptions. Finally the public is realizing the illusory nature of the market run-up, cognizant that their own household micro-economy has not followed suit. Could it be the approximate $100 billion in funny money per month that the Federal Reserve (Fed) is pumping into the markets? Probably. And the best evidence yet that this is the case is the recent market drop due to falling unemployment rates. Yes, you read that right.

Usually falling unemployment means higher consumer disposable income and therefore higher spending which in turn buoys corporate earnings, causing stock values to rise. So why are they falling instead?? Because Wall Street fears the Fed will back off on its Monopoly money stimulus as the jobs picture "improves" (It's not improving, not really. They're just measuring it differently.). Less money chasing the same securities will cause stock prices to fall. Hence the defensive sell off now.

Wall Street's mantra is "You don't want to miss the best days of the market, so keep fully invested". My mantra is, "It is far more important to avoid the worst days!"

Saturday, July 27, 2013

Obamacare is Bad (to be clear, this is mostly a myth)

The best way to counter any mass mythology is with specific, factual information. The degree of misinformation, hysteria and outright sabotage surrounding the Affordable Care Act (aka Obamacare) seems unprecedented in recent history. Too many powerful people will harm as many others as necessary simply for political advantage. Ironically, Obamacare is a very flawed piece of legislation largely because of these deranged people. Compromise with them was necessary to get this landmark law passed.* But the majority of us are good, decent and want the best for our fellow citizens. And we managed to get dozens of good provisions into Obmacare.

The Patient-Centered Outcomes Research Institute (PCORI) is a wonderful example of specific reality to counter those who inexplicably attack the Affordable Care Act, thereby shooting themselves in the feet. At a cost of about $2 per person per year, PCORI:

". . .helps people make informed health care decisions, and improves health care delivery and outcomes, by producing and promoting high integrity, evidence-based information that comes from research guided by patients, caregivers and the broader health care community."

And better yet, PICOR doesn't attempt to implement this vision with a top-down bureaucratic strategy. Instead it funds carefully selected research projects all over the country. Regrettably, some states saddled with obtuse leadership are actually refusing this funding. Oregon is not one of them!

So do your own research, believe the opposite of what you hear on FOX, and please visit your local state exchanges (i.e. if your State cares about you). Oregon's is www.coveroregon.com

*all that was really necessary was a single sentence amendment to the Medicare laws, rather than a 1400+ page bill: Any citizen of any age may enroll in Federal Medicare. That would have saved employers 30-50% on their employee benefits expenses.

The Patient-Centered Outcomes Research Institute (PCORI) is a wonderful example of specific reality to counter those who inexplicably attack the Affordable Care Act, thereby shooting themselves in the feet. At a cost of about $2 per person per year, PCORI:

". . .helps people make informed health care decisions, and improves health care delivery and outcomes, by producing and promoting high integrity, evidence-based information that comes from research guided by patients, caregivers and the broader health care community."

And better yet, PICOR doesn't attempt to implement this vision with a top-down bureaucratic strategy. Instead it funds carefully selected research projects all over the country. Regrettably, some states saddled with obtuse leadership are actually refusing this funding. Oregon is not one of them!

So do your own research, believe the opposite of what you hear on FOX, and please visit your local state exchanges (i.e. if your State cares about you). Oregon's is www.coveroregon.com

*all that was really necessary was a single sentence amendment to the Medicare laws, rather than a 1400+ page bill: Any citizen of any age may enroll in Federal Medicare. That would have saved employers 30-50% on their employee benefits expenses.

I WOULD NEVER BE IN SALES

Every once in a while a book comes along that is refreshing, groundbreaking and fun to read. Dan Pink's new book, "To Sell Is Human, the surprising truth about moving others", is one of those books. I highly recommend it to anyone who is not a hermit.

My dad was a chemistry professor at Willamette University. So I acquired a mild to blazing condescension to salespeople. Yet, Dad ignored the fact that his occupation consisted almost entirely of "selling" chemistry knowledge to often recalcitrant young students. His job was to move them towards an "A" in chemistry if at all possible. He enjoyed it immensely. And he was very good at it. But by god it wasn't sales.

So I'm sure there was some disappointment when I became an insurance agent. Since those were the good old days of cold calling, I had descended into the dregs of sales: dinner time telephone solicitation for insurance "x-dates". Believe it or not, I called out of the white pages, "Good evening Mr. _____, this is Gary Duell with Farmers Insurance. Would you be interested in comparing with us when your next insurance policy renewal comes up?" If on the off chance they were willing, I would collect as many details as possible on my X-date card and file it by date for future contact. I remember cheering and dancing around the "boiler" room when I got my first X-date. And went on to collect over 2000 of them. Hardly good use for an MBA.

Without revealing too much of Pink's excellent book, I can say that he turns the classical sales model on its head. ABC- always, be, closing, becomes ABC- attunement, boyancy & clarity. His research shows how sales actually is a very honorable profession, while some very honorable professions are actually sales. I highly recommend it!

My dad was a chemistry professor at Willamette University. So I acquired a mild to blazing condescension to salespeople. Yet, Dad ignored the fact that his occupation consisted almost entirely of "selling" chemistry knowledge to often recalcitrant young students. His job was to move them towards an "A" in chemistry if at all possible. He enjoyed it immensely. And he was very good at it. But by god it wasn't sales.

So I'm sure there was some disappointment when I became an insurance agent. Since those were the good old days of cold calling, I had descended into the dregs of sales: dinner time telephone solicitation for insurance "x-dates". Believe it or not, I called out of the white pages, "Good evening Mr. _____, this is Gary Duell with Farmers Insurance. Would you be interested in comparing with us when your next insurance policy renewal comes up?" If on the off chance they were willing, I would collect as many details as possible on my X-date card and file it by date for future contact. I remember cheering and dancing around the "boiler" room when I got my first X-date. And went on to collect over 2000 of them. Hardly good use for an MBA.

Without revealing too much of Pink's excellent book, I can say that he turns the classical sales model on its head. ABC- always, be, closing, becomes ABC- attunement, boyancy & clarity. His research shows how sales actually is a very honorable profession, while some very honorable professions are actually sales. I highly recommend it!

Wednesday, June 19, 2013

You can fool some of the people all of the time but . . .

Online newsletter OnWallStreet tells us that in May, $56 billion of net inflows (new investments less redemptions) were attracted by stock and bond mutual funds & ETFs. Which brings the total so far thru May to $350 billion. Now that may not seem like a very large number compared to the $13 trillion held by U.S. Investment Companies (mutual fund families). But it bothers me; people are still chasing returns at the top of the market, believing Wall Street's mythology that somehow the economy is "on the road to recovery". Keep this in mind: someone else is selling those shares.

Monday, June 10, 2013

Students, no financial risks this Summer- MYTH

Financial tips for college graduates

(With a few edits, the entirety of this post is from the Oregon Department of Consumer & Business Services. Very well done.)

Here are financial tips in a few key areas:

Health insurance: If you land a job that doesn't offer insurance, remember that you can stay on your parents’ plan until age 26 – and you do not have to live at home, be a student, or be a dependent on your parents’ tax return. You may also buy an individual policy directly from an insurance company or through an agent. As of Jan. 1, 2014, many young people will qualify for Medicaid, the state health insurance program, or subsidies to help pay for private insurance. Visit www.coveroregon.com starting in October to shop.

Credit rating: Go easy on the credit cards. Your credit score will follow you. A poor score may force you to pay more or result in rejection for everything from insurance to a home loan to credit cards. If you need help managing debt, the Division of Finance and Corporate Securities can help you find a licensed and certified nonprofit credit counselor. Call 503-378-4140. Meanwhile, the federal Consumer Financial Protection Bureau has lots of information about credit scoring. [And on the other hand, to build a credit score you need to incur some debt. I recommend a very low limit credit card that pays points and which you pay off every month. GD]

Start saving: Even though you may have little left over after paying bills, putting away even a small amount starts a habit that will pay big dividends later. More than half of Americans said they are worried about a lack of savings, according to an annual Financial Literacy Survey conducted by two nonprofit organizations. This page links to tools that explain how to save: http://www.cbs.state.or.us/dfcs/investor_info_program/america_saves.html.

[On the other hand, if you have any debt- especially any debt costing you an interest rate higher than you can safely earn -pay that down first. GD]

Renter insurance: If fire destroys your rental apartment or house, the owner’s policy will cover the structure but not your contents. If you have a lot of electronics or other expensive items, or if you lack the money to replace what you do have, you may want renter insurance. The cost averages less than $15 a month in Oregon. And, it covers your personal liability if someone is injured because of your activities on or off your premises (say your dog bites someone). [Perhaps even more likely to happen is your inadvertent damage to the building, which is also covered to varying degrees, depending on the company. Most policies cover your possessions anywhere, not just in your apartment. (be mindful, however, of exclusions and limitations- ask your agent!) And if you already have car insurance on your own, adding a Renter's Package may give you discount on your car premium. GD].

Help with finance questions: The Department of Consumer and Business Services regulates many financial services and industries. Consumer insurance advocates can answer insurance questions and are available from 8 a.m. to 5 p.m. Monday through Friday. Call toll-free in Oregon: 888-877-4894. If you have questions about consumer loans or people offering to help you manage debt, the Division of Finance and Corporate Securities can help. Call 503-378-4140. [Or, if you want greater expertise, call me. GD]

The Department of Consumer and Business Services is Oregon’s largest business regulatory and consumer protection agency. Visit www.dcbs.oregon.gov. Follow DCBS on Twitter: http://twitter.com/OregonDCBS. Receive consumer help and information on insurance, mortgages, investments, workplace safety, and more.

Friday, May 31, 2013

I AM TOO CONSERVATIVE

Before I get started, two caveats are in order:

- Remember that these blog titles are Myths.

- By "conservative" I mean in terms of your financial security. Politically I range from a Teapartier to a bleeding heart Liberal, depending on the issue.

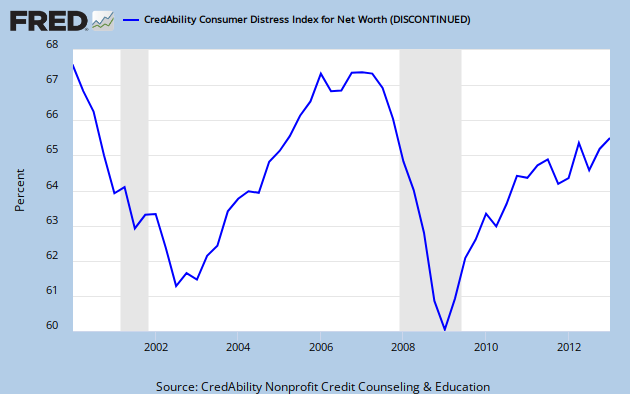

First, take a look at this fascinating graph (I know. That may be an oxymoron):

(If you can't read the small print, or if you would like to tweak the parameters yourself, click on the link directly below the graph.) I love graphs because they make the invisible visible, the complicated simple, the hazy, clear. Beginning in the year 2000 this graph measures 50 different data points which reflect consumer confidence. The lower the score, the lower the level of "Consumer Distress". The key take away: note the peak in consumer confidence (i.e., lack of distress) just before each market crash. Yet mildly rising consumer confidence is touted in the press as reason for optimism. Which of course is circular thinking, "We should be optimistic because we are optimistic". Sounds stupid when I put it that way doesn't it?

But here are the facts which should sober up your drunken revelry about the "record" stock market indices. First of all, Americans lost $16 trillion in household wealth in the Bush recession. It appears we've just about gotten it back. But secondly, unless you factor in inflation & the increase in the number of households, you're dreaming. The average family is only about halfway recovered and would need to double current asset values in order to be "even". Ain't gonna happen. Not because of consumer confidence.

My point here is not to put my elbow in the party cake. My point is to emphasize the importance of not losing money. Risk management is not only more important than chasing the Wall Street casino but it is also the only factor that is in your control. This is both conservative and optimistic: if you can reduce risk and have sufficient retirement income, why gamble with your future?? Why gamble at all?

Saturday, May 25, 2013

CAN YOU DO IT YOURSELF?

Retirement planning consists of much more than maximizing investment returns. I think risk management is far more important. And difficult. Sure, you may be able to do a great job all by yourself. But would it be worth $49 to see if you have what it takes, and, to be sure you leave no stone unturned?

My next series of Retirement Planning courses begins this May 30th, 6:30-8:30pm. The materials & ideas presented are based on academic research; this is not in any way a sales presentation. Student evaluations have been "Excellent". And I've included a lot of humor to keep it interesting.

For your tuition you will receive:

Or call me at 503-698-1110

Gary

My next series of Retirement Planning courses begins this May 30th, 6:30-8:30pm. The materials & ideas presented are based on academic research; this is not in any way a sales presentation. Student evaluations have been "Excellent". And I've included a lot of humor to keep it interesting.

For your tuition you will receive:

- Financial House in Order Guidebook

- Managing Your Money in Retirement Guide

- Getting Your Estate in Order Guide- this is a wonderful resource

- Personal Wealth Index Scores/Report-it's not all about money. Life is more than a math problem.

- Social Security Analysis Report- avoid the most common HUGE, irreversible mistake I encounter.

- Course Workbook and Essential Reports

- Optimal Asset Allocation in Retirement

- Defining Core Priorities

- How Money Affects Your Life

- How to Develop an Income Plan

- Sequence of Returns Risk

- Questions to Ask a Potential Adviser

- When to Take Social Security

- 3 Reasons Retirees Run Out of Money

Or call me at 503-698-1110

Gary

Sunday, May 12, 2013

AARP is a reliable source of financial advice & evidence based public policy.

Once again, lest there be any doubt, the title of this post is a MYTH. Current case in point is the recent AARP "BULLETIN" titled "Now's the Time for Tax Reform", written by Nina E. Olson, "National Taxpayer Advocate". Not. That is, if this is our advocate, who needs an adversary?

The upshot of Ms. Olson's article is that we have met the enemy of tax reform. And it is us. Because we average Americans greedily cling to our "special interest" deductions such as mortgage interest and medical expenses. She opines we must be willing to give up these deductions in exchange for "comprehensive simplification"of the tax code. The underlying presumption is that the complexity of the tax code causes "high" tax rates and simplification will cause our taxes to go down.

This is of course total nonsense. And it is embarrassing (but not surprising) to read it in a massive marketing organization's (that's what AARP is) newspaper. Here's why:

The upshot of Ms. Olson's article is that we have met the enemy of tax reform. And it is us. Because we average Americans greedily cling to our "special interest" deductions such as mortgage interest and medical expenses. She opines we must be willing to give up these deductions in exchange for "comprehensive simplification"of the tax code. The underlying presumption is that the complexity of the tax code causes "high" tax rates and simplification will cause our taxes to go down.

This is of course total nonsense. And it is embarrassing (but not surprising) to read it in a massive marketing organization's (that's what AARP is) newspaper. Here's why:

- The problem is not complexity. That may have been the case before computers were invented. They can handle it now. Complexity is simply a symptom of the real problem. The most powerful interests keep slipping abusive provisions into the tax code, which our few remaining ethical lawmakers then attempt to fix. Which lobbyists then try to undo. And so on. This vicious cycle is responsible for the malignant growth of the tax code. Ms. Olson cites required minimum distribution rules and Social Security taxation as examples of how tax complexity baffles seniors. But just about anyone can figure them out.

- The problem is inequity, that is, those who benefit most from government expenditures contribute the least to the Treasury, measured as a percent of their income. No, I'm not talking about welfare cheats or those naughty seniors who keep whining for their meds so they can stay alive.

- The cheaters, the "winners" in the tax game are:

a. Those wealthy individuals who are hiding $11.5 trillion off shore, strictly to avoid Federal, State and local taxes. See http://www.taxjustice.net/cms/front_content.php?idcat=2

b. Corporations are more difficult to assess. Nobody seems to know the exact total trillions offshored by them. It seems reasonable to guess that the total of individual and corporate tax dodging exceeds the entire GDP of the United States.

Friday, April 26, 2013

Myth: The Stock Market will always out-perform all other investment options

Yours truly used to spout this myth when I worked for broker-dealers, before I became an independent Registered Investment Adviser (yes, regulations dictate adviser be spelled "'er" not "'or"). And in practically the same breath we uttered the caveat, "past performance is no guarantee of future results". That's how we were trained to mislead the public. But can anyone tell me how in the world those two statements fit together?? What if I am looking for guarantees? Are there any left that are worth examining? Of course there are. But here's the key: ethical risk transference.

I added that pesky word "ethical" because the vast majority of risk is transferred to those unwilling to assume it. Taxpayer bailouts of the wealthiest people and companies in the world are a good example. Profits are privatized. Losses are socialized.

Taking on risk should be voluntary. Fortunately, there are entities and individuals still willing to take all market risk off your shoulders.

I added that pesky word "ethical" because the vast majority of risk is transferred to those unwilling to assume it. Taxpayer bailouts of the wealthiest people and companies in the world are a good example. Profits are privatized. Losses are socialized.

Taking on risk should be voluntary. Fortunately, there are entities and individuals still willing to take all market risk off your shoulders.

Thursday, April 25, 2013

WE'RE IN AN ECONOMIC RECOVERY

Is the economy recovering? I don't think so, not as evidenced by a market buoyed primarily by a couple trillion dollars of newly printed money. But judge for yourself. Pattern recognition is supposed to be one sign of cognitive intelligence. What do you think of this pattern?

S&P 500 Since Inception

Note the peaks just before the big crashes in 2002 & 2008. And this peak is even more artificial than those. Wouldn't it make sense to prepare for the possibility that we're due for another even more severe burst bubble? It is possible to lock in your gains and even participate in continuing market growth should that unlikely prospect occur? Yes, it is not only possible but quite easy. But not if you stay fully invested in today's foamy, smoke & mirrors, yeehah market. Recent studies indicate that retirees should have, at most, 10-15% at risk in securities, which includes stocks, bonds and mutual funds investing in them. How should your retirement assets be positioned?

S&P 500 Since Inception

Note the peaks just before the big crashes in 2002 & 2008. And this peak is even more artificial than those. Wouldn't it make sense to prepare for the possibility that we're due for another even more severe burst bubble? It is possible to lock in your gains and even participate in continuing market growth should that unlikely prospect occur? Yes, it is not only possible but quite easy. But not if you stay fully invested in today's foamy, smoke & mirrors, yeehah market. Recent studies indicate that retirees should have, at most, 10-15% at risk in securities, which includes stocks, bonds and mutual funds investing in them. How should your retirement assets be positioned?

Wednesday, April 10, 2013

MYTH: Celebity investment "Advisers" outperform the rest

I am severely biased on this topic but recent research shows that "retirees who work with financial planners can get more mileage from their retirement portfolios - approximately 1.82% higher returns during retirement." Even though that is true, on average, investment returns are the least important value we advisers provide to our clients!

In an excellent summary of the issue in Advisor Perspective, Bob Veres opines,

"Jim Cramer, Suze Orman and other so-called investment pundits and gurus are constantly telling consumers that they can do a great job of managing their portfolios on their own. Why pay a fee for professional asset management when you can turn on the TV and get Cramer's stock-picking expertise for free?"

Veres goes on to quantify the huge value that holistic advisers (as opposed to product pushers masquerading as "planners" or celebrity "advisers" peddling financial porn) generate for their clients, ranging from annualized 4-8% better long term performance. Yes. 4-8%! On the other hand, the average investor costs himself 2% per year versus unmanaged indexes. Granted, exceptions abound. But if you're "average" why not employ a planner? Most of us pay for ourselves many many times over. Here's how, according to Veres:

"Mark Hulbert has compared the overall performance of Cramer's Action Alerts with the Wilshire 5000 index for the calendar years 2009, 2010 and 2011. (You can find the chart here). Hulbert found that over the three-year period, Cramer's recommendations would have delivered an investment performance of roughly 9.9% a year – and this did not account for trading costs or tax obligations that accumulate when you're buying and selling 10 or 11 times a day. During the same time period, the Wilshire 5,000 [unmanaged] index delivered an average annual return of 14.9%."

Yes, I'm more boring than Jim Cramer. But I'll bet you'll be better off in the long run. Even the short run!

Gary

In an excellent summary of the issue in Advisor Perspective, Bob Veres opines,

"Jim Cramer, Suze Orman and other so-called investment pundits and gurus are constantly telling consumers that they can do a great job of managing their portfolios on their own. Why pay a fee for professional asset management when you can turn on the TV and get Cramer's stock-picking expertise for free?"

Veres goes on to quantify the huge value that holistic advisers (as opposed to product pushers masquerading as "planners" or celebrity "advisers" peddling financial porn) generate for their clients, ranging from annualized 4-8% better long term performance. Yes. 4-8%! On the other hand, the average investor costs himself 2% per year versus unmanaged indexes. Granted, exceptions abound. But if you're "average" why not employ a planner? Most of us pay for ourselves many many times over. Here's how, according to Veres:

- We keep you from chasing the next hot stock or fund just before it tanks.

- We make sure you stick with your asset allocation by employing at least twice yearly rebalancing

- We help define and implement diversification on many levels. Veres only discusses investment diversification but it is also important to have health, interest rate and inflation diversification, to name a few other risks in addition to volatility.

- We consider and prepare for taxation. The types and timing of assets acquired and income taken must be framed in your unique current and expected tax picture.

- On average, we compel you to not only save more but smarter (usually with tax advantages).

"Mark Hulbert has compared the overall performance of Cramer's Action Alerts with the Wilshire 5000 index for the calendar years 2009, 2010 and 2011. (You can find the chart here). Hulbert found that over the three-year period, Cramer's recommendations would have delivered an investment performance of roughly 9.9% a year – and this did not account for trading costs or tax obligations that accumulate when you're buying and selling 10 or 11 times a day. During the same time period, the Wilshire 5,000 [unmanaged] index delivered an average annual return of 14.9%."

Yes, I'm more boring than Jim Cramer. But I'll bet you'll be better off in the long run. Even the short run!

Gary

Monday, February 4, 2013

MYTH: We don't like risk.

I used to have five chickens, Stella, Sophie, Sam, Gertrude and Emma. Gertrude died of cancer. Emma, Sam and Sophie filled the bellies of the local coyotes, one by one and in that order. So I'm left with Stella, my least favorite. STELLAAA!!

How could you have a least favorite chicken, you ask? Well, my favorite, Sam, was a beautiful Black Sexton with big brown eyes and an inquisitive, friendly disposition. She was the only one who would let me pick her up. She was the only one who would be practically under foot while I was weeding, ready to pounce on worm and bug. Stella, on the other hand, was downright obtuse. I would throw out a handful of popcorn duds- one of the their favorite treats -and while her sisters would dash over to gobble them up she would linger at a distance until it was too late. She would never let me get close to her. I thought she was simply dumb.

But the other day when I tried to herd her into the coop, she adeptly evaded me with the circle-around-the-bush technique. Then it dawned on me: She's the one who is still alive.

We seem hold the same illusions about our investments, preferring the "friendly" ones even though they don't serve us well. Shouldn't it be a clue, the billions Wall Street spends on convincing us to let them keep using and losing our money? Unfortunately, we like the risks that we're told to like, the risks that are heavily marketed to us as the prerequisites to making it big.

How could you have a least favorite chicken, you ask? Well, my favorite, Sam, was a beautiful Black Sexton with big brown eyes and an inquisitive, friendly disposition. She was the only one who would let me pick her up. She was the only one who would be practically under foot while I was weeding, ready to pounce on worm and bug. Stella, on the other hand, was downright obtuse. I would throw out a handful of popcorn duds- one of the their favorite treats -and while her sisters would dash over to gobble them up she would linger at a distance until it was too late. She would never let me get close to her. I thought she was simply dumb.

But the other day when I tried to herd her into the coop, she adeptly evaded me with the circle-around-the-bush technique. Then it dawned on me: She's the one who is still alive.

We seem hold the same illusions about our investments, preferring the "friendly" ones even though they don't serve us well. Shouldn't it be a clue, the billions Wall Street spends on convincing us to let them keep using and losing our money? Unfortunately, we like the risks that we're told to like, the risks that are heavily marketed to us as the prerequisites to making it big.

Monday, January 14, 2013

Myth: Social Security is in Trouble

Financially, this blog title is a myth. Politically it is not. An absolutely excellent article on AlterNet by Lynn Stuart Parramore is the basis for this post and I will quote it heavily. I had led you to believe I would do a Fiscal Bluff Part II follow up post but I think it has become apparent the world did not come to an end. So I'm saving that for later. Social Security has been part of the Fiscal Bluff debate for inexplicable reasons. Parramore lists those reasons in her article titled, "The Giant Lie Trotted Out by Fiscal Conservatives Trying to Shred Social Security".

Here I list each supposed "problem" with Social Security and the corresponding truth:

Here I list each supposed "problem" with Social Security and the corresponding truth:

- OMG seniors are living so much longer than we expected! They're going to bankrupt the system! THE TRUTH: Social Security's original policymakers quite accurately predicted increasing longevity.

- OMG we need to raise the "normal" (or "full") retirement age as a result! THE TRUTH: In fact, retiree life expectancy gains since 1935 have been modest. Early figures were based on expectancy at birth, not at age 65. Life expectancy at 65 has only increased by 5 years since 1940, from 14.7 years to 19.6 years. Besides, the Full Retirement age has already been increased from 65 to 67 for certain age groups. Unnecessarily. By the Greenspan Commission back in 1983. Remember? Greenspan, the architect of our fiscal disaster.

- OMG we're going to be supporting a sea of broke old people! THE TRUTH: Longevity gains have gone to the affluent. Among the poorer and less educated, women have lost 5 years, men 3 years. Out of 34 industrialized countries we rank 27th in life expectancy. So as Parramore points out, raising the retirement age again would be a "direct assault" on the less fortunate. Furthermore, life expectancy gains are expected to slow in the future.

Monday, December 17, 2012

"Fiscal Cliff" or Fiscal BLUFF?

Do you think Congress is totally partisan? (Note to my Tea Party impaired friends, "partisan" means "prejudiced in favor of a particular cause", that is, either Democratic or Republican in this case. It does not mean, "Contrary to my current beliefs".) Partisanship has been most dramatically manifested by the Republicans voting lockstep against any Democratic proposals regardless of merit, some of which they once supported or even invented themselves! Even so, I don't think they're uniquely partisan. Because the one issue both parties agree upon is kowtowing to the super rich.

Let me define "super rich". A super rich person already has so much wealth that his lifetime material security is guaranteed. The pathologically super rich, though, become unhappy if their wealth fails to increase every moment in time. Any involuntary cost, even though it will have zero lifestyle impact, even though it might actually benefit them, is tantamount to a physical assault. This includes taxation. (Whether this arises from overly controlling parents, or not being held enough as infants, we can only speculate.) Those who benefit from the Golden Goose that lays their golden eggs, the infrastructure that makes wealth possible, need to help feed the goose. It is impossible to single handedly create wealth in a vacuum. But neither party seems to have the guts to ask these folks for sufficient revenue to protect and build our Commons. (Yes, that's capital "C" Commons. Please review the definition.)

Which brings us to the topic at hand, the fabricated myth of The Fiscal Cliff, lions, tigers and bears, oh my! (Will we ever develop immunity to irrational, baseless fears?) "The Fiscal Cliff" rolls off the tongues of pundits in every media with little explanation of what the hell it actually is or why, or even if, it is a bad thing. Personally, I think we should let "it" happen and I'll explain what "it" is in a moment. But before that, start thinking of The Fiscal Cliff instead as a snowy Fiscal Bluff over which we're about to take a fun glide on our Fiscal Sleds, ("Bluff" being an intentional double entendre). The Fiscal Cliff is an exaggerated, astoundingly nationalistic & partially manufactured distraction from vastly more serious issues such as the poisoning of everything we ingest & global climate change. issues nobody wants to deal with until it is too late. Which it probably already is. But . . .

To put it simply, our economy will tumble over the Fiscal Bluff in January, supposedly, when two job killing events will occur: higher taxes caused by the expiration of the Bush tax giveaways, and, precipitous cuts in government spending. Media and political dufuses somberly lament that this will allegedly send unemployment sky high and the markets into a ravine. You would think an asteroid is hurtling towards us. Some people perversely lust so much for this to be true that they're firing otherwise profitable employees (need I say Papa Johns?).

The first odd thing you will note about these two devilish horns is the implication that government spending creates jobs, which is true with one major exception. The exception is military spending which, although it does create jobs, only creates one-third as many as, say, building a domestic school or bridge. The second odd thing you will note is the implication that taxes create unemployment, which is false with few exceptions. These two views are incompatible. So reality must be somewhere in between.

The details are too lengthy to post here, but that's the beauty of the Internet (which arose from government programs, by the way). Do your own research and don't believe anyone, including me. So, in anticipation of this sleigh ride, what do you do with your money? Stash it in places that will protect it from any market declines but which will also participate in market gains should those occur. Yes, there are such places.

To be continued . . .

Let me define "super rich". A super rich person already has so much wealth that his lifetime material security is guaranteed. The pathologically super rich, though, become unhappy if their wealth fails to increase every moment in time. Any involuntary cost, even though it will have zero lifestyle impact, even though it might actually benefit them, is tantamount to a physical assault. This includes taxation. (Whether this arises from overly controlling parents, or not being held enough as infants, we can only speculate.) Those who benefit from the Golden Goose that lays their golden eggs, the infrastructure that makes wealth possible, need to help feed the goose. It is impossible to single handedly create wealth in a vacuum. But neither party seems to have the guts to ask these folks for sufficient revenue to protect and build our Commons. (Yes, that's capital "C" Commons. Please review the definition.)

Which brings us to the topic at hand, the fabricated myth of The Fiscal Cliff, lions, tigers and bears, oh my! (Will we ever develop immunity to irrational, baseless fears?) "The Fiscal Cliff" rolls off the tongues of pundits in every media with little explanation of what the hell it actually is or why, or even if, it is a bad thing. Personally, I think we should let "it" happen and I'll explain what "it" is in a moment. But before that, start thinking of The Fiscal Cliff instead as a snowy Fiscal Bluff over which we're about to take a fun glide on our Fiscal Sleds, ("Bluff" being an intentional double entendre). The Fiscal Cliff is an exaggerated, astoundingly nationalistic & partially manufactured distraction from vastly more serious issues such as the poisoning of everything we ingest & global climate change. issues nobody wants to deal with until it is too late. Which it probably already is. But . . .

To put it simply, our economy will tumble over the Fiscal Bluff in January, supposedly, when two job killing events will occur: higher taxes caused by the expiration of the Bush tax giveaways, and, precipitous cuts in government spending. Media and political dufuses somberly lament that this will allegedly send unemployment sky high and the markets into a ravine. You would think an asteroid is hurtling towards us. Some people perversely lust so much for this to be true that they're firing otherwise profitable employees (need I say Papa Johns?).

The first odd thing you will note about these two devilish horns is the implication that government spending creates jobs, which is true with one major exception. The exception is military spending which, although it does create jobs, only creates one-third as many as, say, building a domestic school or bridge. The second odd thing you will note is the implication that taxes create unemployment, which is false with few exceptions. These two views are incompatible. So reality must be somewhere in between.

The details are too lengthy to post here, but that's the beauty of the Internet (which arose from government programs, by the way). Do your own research and don't believe anyone, including me. So, in anticipation of this sleigh ride, what do you do with your money? Stash it in places that will protect it from any market declines but which will also participate in market gains should those occur. Yes, there are such places.

To be continued . . .

Friday, October 19, 2012

MYTH: The FDIC has 99 years to pay claims

I'm not sure where this myth originated nor do I really care. But it is a myth indeed. (I suspect either anti-government zealots and/or crooks selling "better" savings vehicles.) The fact is that FDIC regulations require the FDIC to replace lost bank deposits "as soon as possible " (see 12 USC1821(f)), usually the next day.

The FDIC was formed in response to the bank failures of the Great Depression (no, not this one, the one in 1929), Prozac for the banking system so to speak. I think it was a mistake because one artifact of safety nets such as the FDIC is that those with moral weakness (aka "humans") might tend to take more risks than they would in the absence of the insurance.

For example, imagine a football game with no referees. Instead there is just Game Insurance so that whichever team loses the game actually gets to win. Both teams win! Cheating & incompetence don't matter! How hard would either team try if that were the case?? I would prefer strict rules strictly enforced, with real penalties, which is how football is conducted now. Anybody know of a Wall Street banker who has been jailed since 2008? I don't. Where are the hundreds of heads that should be rolling from AIG, Lehman, & Countrywide, to name a few? The only things that are rolling are their companies' executives . . . in cash. Win win.

But back to the topic, the FDIC is indeed an important safety net for those of us here at the bottom of the food chain. And a married couple can easily enjoy a million dollars of protection. At the same bank. Each may have an IRA and an savings account insured up to $250k per account.

Having said that, keep in mind that there is no risk-free investment or savings vehicle. Let me say that another way. There is no risk-free investment or savings vehicle. (Do a google search for "financial risk" to review the different types of risk.) This is important enough to say a third way: There is no risk-free investment or savings vehicle. Here's why.

Although CDs and bank accounts are FDIC insured, they guarantee that you'll be subject to inflation certainty. Not inflation risk ("risk" is when you're unsure whether or not an event will occur.), inflation certainty because inflation will certainly exceed the returns your bank can offer.

So ultimately, the types of financial risk you need to minimize depend on what order you rank the four main financial priorities for a portfolio:

The FDIC was formed in response to the bank failures of the Great Depression (no, not this one, the one in 1929), Prozac for the banking system so to speak. I think it was a mistake because one artifact of safety nets such as the FDIC is that those with moral weakness (aka "humans") might tend to take more risks than they would in the absence of the insurance.

For example, imagine a football game with no referees. Instead there is just Game Insurance so that whichever team loses the game actually gets to win. Both teams win! Cheating & incompetence don't matter! How hard would either team try if that were the case?? I would prefer strict rules strictly enforced, with real penalties, which is how football is conducted now. Anybody know of a Wall Street banker who has been jailed since 2008? I don't. Where are the hundreds of heads that should be rolling from AIG, Lehman, & Countrywide, to name a few? The only things that are rolling are their companies' executives . . . in cash. Win win.

But back to the topic, the FDIC is indeed an important safety net for those of us here at the bottom of the food chain. And a married couple can easily enjoy a million dollars of protection. At the same bank. Each may have an IRA and an savings account insured up to $250k per account.

Having said that, keep in mind that there is no risk-free investment or savings vehicle. Let me say that another way. There is no risk-free investment or savings vehicle. (Do a google search for "financial risk" to review the different types of risk.) This is important enough to say a third way: There is no risk-free investment or savings vehicle. Here's why.

Although CDs and bank accounts are FDIC insured, they guarantee that you'll be subject to inflation certainty. Not inflation risk ("risk" is when you're unsure whether or not an event will occur.), inflation certainty because inflation will certainly exceed the returns your bank can offer.

So ultimately, the types of financial risk you need to minimize depend on what order you rank the four main financial priorities for a portfolio:

- Preservation

- Income

- Liquidity

- Growth

Sunday, September 2, 2012

MYTH: The Best Place Is a Money Milkshake!

The most frequent question posed to me by clients, friends & new contacts is this: "Where's the best place to put my money?" I'll get to the presumptions behind this question in a minute. But it cannot be honestly answered without more information.

I usually say, "Well, it depends on what you want, what your plans are, your current asset level, when you want to retire, your pre & post-retirement budget, how long you expect to live, your debt level, your rate of return history and expectations, your risk tolerance, your health, your wishes for your family or charities . . " and so on. Sometimes though, if I'm feeling flippant, I'll say something like "It all depends on what you want. If you want a money milkshake, the best place for your money is in a blender with vanilla ice cream and blueberries." I'm sure, more often than not, that feels evasive, like I'm dodging the issue.

So what are people thinking when they pose that question? I suspect most have in the backs of their minds that authoritative but fickle pie chart that shows up on their brokerage/retirement statements. You know, similar to these:

Looking backwards, they are painfully aware that if only they had adjusted those pieces of the pie, they would have made a ton of money rather than losing. Or, if they hadn't been so conservative, they would have at least kept up with inflation. They blame themselves for responding- or not responding -to Wall Street's siren call. "Now is always a good time to invest!" as TV's financial guru (not) Cramer screams. But they shouldn't blame themselves. Over the 20 years ending 12/31/2010, average equity fund investors earned 3.83%/yr. The S&P500 index earned 9.14%! The problem is chasing returns, buying high and selling low, and incurring too many expenses. (And then there's the issue of the shrinking number of fund managers who actually beat the unmanaged indexes. As financial data becomes more and more accessible, only about 15% of managers beat the indexes to which their styles are compared.)

But why settle for even the S&P500 returns? Below is a rather complicated graph but it's very important. It shows RISK (defined as how wildly your account balance swings up and down over time) and RETURN (the average annual return over the 10 year period shown) for the S&P500 vs. Vanguard. Note how much better Vanguard's unmanaged, low cost index portfolios outperform the S&P500 at large. Even so, can we rely on the past to predict the future?

So embedded in the question, "Where is the best place to put my money." is this one: "Where can I get the highest returns without any risk?" What is it perhaps more important to ask? Because the key is asking the right questions. In addition to those posed in my second paragraph, these additional money questions are essential:

Best Always,

Gary

I usually say, "Well, it depends on what you want, what your plans are, your current asset level, when you want to retire, your pre & post-retirement budget, how long you expect to live, your debt level, your rate of return history and expectations, your risk tolerance, your health, your wishes for your family or charities . . " and so on. Sometimes though, if I'm feeling flippant, I'll say something like "It all depends on what you want. If you want a money milkshake, the best place for your money is in a blender with vanilla ice cream and blueberries." I'm sure, more often than not, that feels evasive, like I'm dodging the issue.

So what are people thinking when they pose that question? I suspect most have in the backs of their minds that authoritative but fickle pie chart that shows up on their brokerage/retirement statements. You know, similar to these:

Looking backwards, they are painfully aware that if only they had adjusted those pieces of the pie, they would have made a ton of money rather than losing. Or, if they hadn't been so conservative, they would have at least kept up with inflation. They blame themselves for responding- or not responding -to Wall Street's siren call. "Now is always a good time to invest!" as TV's financial guru (not) Cramer screams. But they shouldn't blame themselves. Over the 20 years ending 12/31/2010, average equity fund investors earned 3.83%/yr. The S&P500 index earned 9.14%! The problem is chasing returns, buying high and selling low, and incurring too many expenses. (And then there's the issue of the shrinking number of fund managers who actually beat the unmanaged indexes. As financial data becomes more and more accessible, only about 15% of managers beat the indexes to which their styles are compared.)

But why settle for even the S&P500 returns? Below is a rather complicated graph but it's very important. It shows RISK (defined as how wildly your account balance swings up and down over time) and RETURN (the average annual return over the 10 year period shown) for the S&P500 vs. Vanguard. Note how much better Vanguard's unmanaged, low cost index portfolios outperform the S&P500 at large. Even so, can we rely on the past to predict the future?

So embedded in the question, "Where is the best place to put my money." is this one: "Where can I get the highest returns without any risk?" What is it perhaps more important to ask? Because the key is asking the right questions. In addition to those posed in my second paragraph, these additional money questions are essential:

- How can I minimize my costs? How can I get my money's worth for the fees I'm paying?

- How can I eliminate risk without taking a bath on poor returns?

- How should I best hold my invested assets (in qualified retirement accounts, real estate, hybrid products, trusts?) to be sure my plans are fulfilled?

- What trends may make historical performance a permanent thing of the past? What is reasonable to expect in the rapidly changing future?

Best Always,

Gary

Saturday, August 11, 2012

The First Thing They Teach Lifeguards

I just returned from a two-day conference with my field marketing organization Wealth Financial Group, based in Chicago. Beautiful city!

Our keynote speaker was author & consultant Frank Maselli, a dynamic, animated, hilarious, brilliant man. Frank likened us financial advisers to lifeguards, trying to convince potential drowning victims to climb into the lifeboat while there is still room. He asked us, "What is the first thing a lifeguard has to learn? To keep from being pulled under by the person you're trying to rescue!".

So true. And it highlighted the stunning frustration most of us non-Wall Street advisers feel as we holler, "Get in the boat! Get in the boat!". The general public has been splashed, dunked, slapped and- in some cases -actually drowned by Wall Street while Wall Streeters accumulate record, massive wealth.

As Nobel prize winning economist Joseph Stiglitz has stated, the economy is broken when financial rewards are disconnected from public benefit. That is, you should not make a lot of money unless you've provided a lot of benefit.

I get paid very well for what I do. Mine is a complicated, rapidly changing, essential business. I put my heart and soul into it and have for over 30 years. It is my professional mission to dispel the Wall Street myth that you have to lose money to make money. I can't believe anyone still buys that shell game. The lifeboat analogy is right on because- as I pointed out in my last blog post -the options for reducing financial risk keep shrinking in number and in quality. The lifeboats are filling up. And I am focusing on swimmers who are close by and ready to climb in.

Our keynote speaker was author & consultant Frank Maselli, a dynamic, animated, hilarious, brilliant man. Frank likened us financial advisers to lifeguards, trying to convince potential drowning victims to climb into the lifeboat while there is still room. He asked us, "What is the first thing a lifeguard has to learn? To keep from being pulled under by the person you're trying to rescue!".

So true. And it highlighted the stunning frustration most of us non-Wall Street advisers feel as we holler, "Get in the boat! Get in the boat!". The general public has been splashed, dunked, slapped and- in some cases -actually drowned by Wall Street while Wall Streeters accumulate record, massive wealth.

As Nobel prize winning economist Joseph Stiglitz has stated, the economy is broken when financial rewards are disconnected from public benefit. That is, you should not make a lot of money unless you've provided a lot of benefit.

I get paid very well for what I do. Mine is a complicated, rapidly changing, essential business. I put my heart and soul into it and have for over 30 years. It is my professional mission to dispel the Wall Street myth that you have to lose money to make money. I can't believe anyone still buys that shell game. The lifeboat analogy is right on because- as I pointed out in my last blog post -the options for reducing financial risk keep shrinking in number and in quality. The lifeboats are filling up. And I am focusing on swimmers who are close by and ready to climb in.

Tuesday, July 31, 2012

MYTH: I can always buy Long Term Care insurance later

I know it must be irritating to you. But I won't stop doing it. That is, regaling you of the steadily shrinking options for reducing your financial risks. The quantity and quality of techniques to protect yourself and your money are in an entropic spiral.

For example, I've mass emailed ad nauseum about the financial safe haven of annuities (which, not surprisingly, the Wall Street owned corporate press continue to trash). My best company, Aviva, just reduced their minimum interest rate to 1%, making it not much better than the average CD (if it weren't for the additional benefits of tax deferral and guaranteed income).

Long Term Care risk management strategies have also been dragged onto the chopping block virtually every month. Several big names have pulled out of the market altogether, such as Prudential and MetLife. Others have discontinued lifetime benefits and what are called "limited pay" premium schedules. Used to be that you could pay larger fixed premiums for 10-20 years thereby eliminating the risk of future rate increases. All have increased their rates on new applicants and existing policyholders alike. My own premiums have doubled in the last 10 years, but are still 1/2 the cost of a similar policy these days. Pays to buy it early!

But sadly, the best buy in Oregon for healthy nonsmokers, United of Omaha, is discontinuing lifetime benefits, group plans, and limited pay options effective with applications signed by tomorrow, August 1. They just told me this today! They also implemented a healthy rate increase a month ago.

What does all this mean? It means that long term care is a serious risk, so serious that it has the insurance companies running scared. The good news is, if properly structured, sufficient protection is still very affordable. With Federal deductibility of premiums and 15% Oregon tax credit, this type of insurance is heavily favored by not only the tax code but several other State and Federal provisions, such as the Partnership Program.

For example, I've mass emailed ad nauseum about the financial safe haven of annuities (which, not surprisingly, the Wall Street owned corporate press continue to trash). My best company, Aviva, just reduced their minimum interest rate to 1%, making it not much better than the average CD (if it weren't for the additional benefits of tax deferral and guaranteed income).