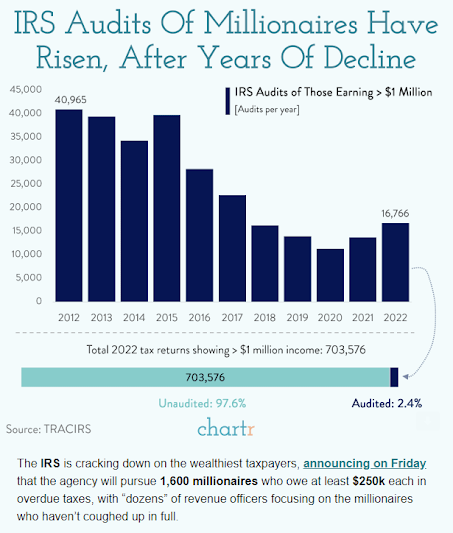

I still feel the need to preface every blog post with the reminder that these blog topic headings are myths, unless I indicate otherwise. It is certainly a myth that our tax systems are fair. Read this carefully, though; this chart doesn't show "Millionaires" as the title suggests. This is individuals and couples who EARN $1,000,000 per year in taxable income. The decline shown from 2012 to 2020 occurred while the number of people in this category skyrocketed.

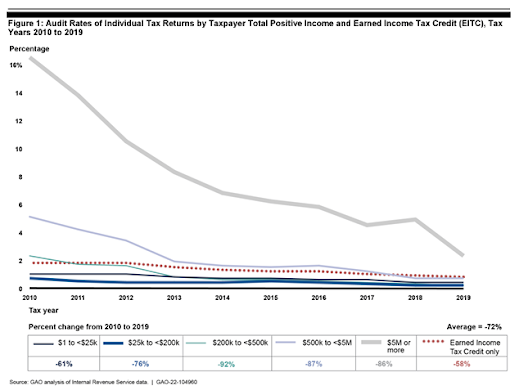

So if you don't have an enrolled agent to do your taxes nor a tax law firm to fight IRS in tax court, you are an easier target. Complex returns are more expensive to audit, especially if they end up in tax court.

We should welcome the Biden administration's increased IRS funding targeting those who owe more than $250,000 in taxes.

But why should we even care? Well, a social and economic system based on merit and equity is simply a happier way to live and such a society is more likely to survive more than a couple hundred years. Our ancestors came over here to escape primarily two plagues: religious persecution, and, a society based on the accumulation of unmerited wealth, usually by inheritance.

But why should we even care? Well, a social and economic system based on merit and equity is simply a happier way to live and such a society is more likely to survive more than a couple hundred years. Our ancestors came over here to escape primarily two plagues: religious persecution, and, a society based on the accumulation of unmerited wealth, usually by inheritance.